AMD: Here's why the stock has 90% upside potential in 2025 (Stock analysis)

On top of AMD's ramp of its data center GPU business, there are other business tailwinds for the company in 2025.

AMD AMD 0.00%↑ is a really interesting business, in my view, and I continue to want to hold the name as an alternative to Nvidia NVDA 0.00%↑ given its inflection in its data center GPU business.

While I think Nvidia will continue to dominate the data center GPU market, I do think there is a place for other competitors like AMD given the size of the market, and given that there is no one-size-fits-all solution.

I also think AMD's diversification beyond data center GPUs, while a headwind today, provides a nice balance to the business in the form of a cyclical recovery in the client business, market share gains in the data center CPU markets and an overall market recovery in the embedded and gaming segments.

Let's dive right into AMD's third quarter.

Third quarter business review

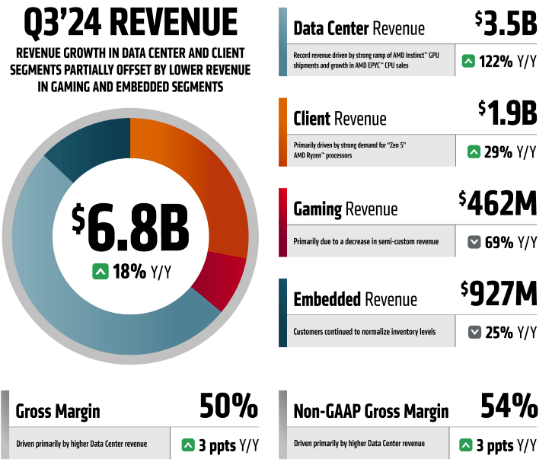

Revenue grew 18% in 3Q24 to reach $6.8 billion, which was 2% ahead of consensus expectations.

Gross margin came in at 54%, expanding 3 percentage points from the prior year and coming in 20 basis points ahead of consensus expectations.

The higher gross margins were contributed by the increase we saw in data center revenues, which will be elaborated on below.

Operating income grew 223% from the prior year to $724 million, largely contributed by the strong growth in the data center segment.

Operating margin came in at 25%, increasing by 21 percentage points from the prior year but coming in 50 basis points below consensus expectations.

This was due to an increase in operating expenses of about 15% due to investment in research and development and go-to-market.

Diluted EPS grew 31% in 3Q24 to reach $0.92 per share, which was in-line with consensus expectations.

I will now go through revenue and operating income by segment.

By segment, as you would expect, data center revenues grew 122% from the prior year to $3.5 billion, beating consensus expectations by 2%.

Client revenues were also strong as the segment grew 29% from the prior year to $1.9 billion, beating consensus expectations by 8%.

The Embedded segment revenue fell 25% from the prior year to $927 million, but still beat expectations by 1%. To be fair, Embedded segment revenue grew by 8% sequentially, which does signal a bottoming of the market.

The Gaming segment revenue fell 69% from the prior year to $462 million, missing consensus expectations by 20% as the Gaming segment continued to face headwinds from lower semi-custom sales given Sony and Microsoft were both trying to bring down their channel inventory.

The main segment contributing to operating income growth is the data center segment. Data center operating income grew 240% from the prior year due to the rapid growth in revenues and the corresponding operating leverage from that.

Data center strength

Data center revenues grew 112% from the prior year, contributed by both data center CPU and GPU revenue growth, which were in turn contributed by server CPU market share gains and the huge ramp in MI300X this quarter.

The ramping of MI300X in the quarter was a key driver for data center GPU revenue growth.

This ramp is high quality in nature, in my view, as hyperscalers are buying MI300X in large quantities for their own internal workloads and for their customers.

Microsoft MSFT 0.00%↑ and Meta Platforms META 0.00%↑ are both known hyperscalers to have publicly announced they will use AMD’s MI300X as an alternative to Nvidia NVDA 0.00%↑ .

As such, they are likely contributing to the ramp in MI300X we are seeing this quarter.

Meta Platforms is leveraging on the MI300X solely for its own internal workloads, namely for managing its internal demand for inferencing, including for its Llama 405 billion parameter model.

On the other hand, Microsoft, as a cloud service provider, is using the MI300X both for internal workloads and public cloud instances.

Microsoft earlier announced that it will offer the MI300X to customers of its cloud computing platform, but Microsoft will also be using it for internal workloads like for their co-pilot services.

Apart from Microsoft, Oracle Cloud Infrastructure is another cloud service provider and hyperscaler providing MI300X to its cloud computing customers this quarter.

AMD is also forging ahead on the software front to keep up with Nvidia by expanding the functionalities on its own software stack for GPU programming, ROCm.

AMD released ROCm 6.2 last quarter, which resulted in some notable benefits, which was mentioned in its 3Q24 earnings call below:

With the release of ROCm 6.2 last quarter, MI300X inferencing performance has improved 2.4 times since launch, and training performance has increased 80%.

We are working closely with a growing number of marquee cloud and enterprise customers to fine-tune their specific inferencing workloads for MI300 with many customers seeing 30% higher performance compared to competitive offerings.

We continue to expand our work with the open-source community, broadening support for key frameworks like JAX, libraries like vLLM and hardware-agnostic compilers like Triton.

Apart from improvements in software, AMD is also looking to acquire companies with complementing capabilities to further leapfrog it against competition.

Last quarter, AMD announced the acquisition of ZT systems, which brings to AMD systems expertise for both rack and cluster level solutions to the company.

AMD is expected to complete the acquisition by the first half of 2025 and sell off the company’s manufacturing business at the same time.

In the earnings call, AMD stated that customer feedback on the acquisition has been positive:

Customer feedback has been very positive as the ZT acquisition enabled hyperscale customers to rapidly deploy AMD AI infrastructure at scale and provides OEMs and ODMs with optimized board and module designs for a wide range of differentiated enterprise solutions.

Lastly, in terms of the data center GPU roadmap, AMD expects MI325X production shipments to begin in the fourth quarter of 2024, with deliveries expected in the subsequent quarter. Management stated that there is strong demand for MI325X from customers.

Further out, after the MI325X, the MI350 is expected to launch in the second half of 2025 while the MI400 is scheduled for launch in 2026.

All in all, demand for its data center GPUs continues to be strong, with revenues revised up from $2 billion at the start of 2024, to $4.5 billion in July, and in October, this number is once again revised up to $5 billion.

In fact, when AMD was asked about 2025 data center GPU outlook, management seemed confident based on their conversations with large customers looking to build their AI infrastructure which means strong demand for data center GPUs, alongside AMD’s strong cadence and innovation each year on this front.

On the negative side, AMD expects its MI300 products to remain margin dilutive for some time. This dilution could continue to weigh on AMD’s stock multiple until they become at least flat with overall gross margins.

In my opinion, I am willing to give AMD time to grow and ramp up the data center GPU business and thereafter, focus on improving gross margins.

Moving to the server CPU market, AMD likely saw market share gains in the third quarter due to an acceleration in the enterprise segment.

Server CPU upside came from the enterprise segment as revenues increased double-digits percentage, the fifth straight quarter of such strong revenue growth within the Enterprise segment. AMD attributed this to strength in the Enterprise segment to “an acceleration in EPYC CPU adoption and growing sell-through momentum". In particular, AMD highlighted that large enterprise customers saw momentum in the quarter across a wide range of verticals.

Of course, the cloud segment continued to be a significant contributor to the server CPU segment, with the largest cloud service providers like Microsoft and AWS expanding to 5th generation EPYC CPU processors.

While data center GPUs have taken the center stage, I think it is important to realize that AMD’s server CPUs are being used in crucial services that are used globally, which was reiterated by AMD below in their earnings call:

In cloud, EPYC CPUs are deployed at scale to power many of the most important services, including Office 365, Facebook, Teams, Salesforce, SAP, Zoom, Uber, Netflix and many more.

Meta alone has deployed more than 1.5 million EPYC CPUs across their global data center fleet to power their social media platforms.

In my opinion, I expect server CPU share gains by AMD to continue due to continued momentum in the enterprise segment, and new product launches and innovation.

Both Google and Oracle Cloud Infrastructure will be launching public cloud instances for fifth-gen EPYC instances early next year and AMD expects broad adoption across its key cloud service provider customers for Turin, which is AMD’s next-generation server CPU.

Turin ramp will be an interesting one to watch as this has been touted as one of the best performing server CPUs available in the market.

This trend of continued expansion in the adoption of AMD’s server CPU processors in the cloud segment continued this quarter as public cloud instances grew 20% from the prior year.

Other segments

The Client segment saw relative strength, with revenues up 29% from the prior year due to Zen 5 notebook and desktop processors.

AMD also launched the AMD’s Ryzen AI Pro 300 Series, which is made for AI PCs and management seems to see that the Ryzen AI Pro is well positioned to gain share as Windows 10 reaches end-of-life status starting in 2025.

Management stated that in the earnings call that “HP and Lenovo are on track to more than triple the number of Ryzen AI Pro platforms they offer in 2024”, and AMD expects to have “more than 100 Ryzen AI Pro commercial platforms in market next year”.

The Embedded segment continued to recover this quarter, but in a more gradual manner. When AMD was asked about 2025 expectations for the Embedded segment, the company maintained relatively conservative expectations believing that it will grow only "modestly".

Gaming was undoubtedly the weakest segment in the third quarter, with continued ongoing inventory digestion with Microsoft and Sony.

AMD will be launching its next-generation RDNA4 GPUs in early 2025, which brings about an improvement in gaming performance.

The gaming segment is expected to remain sluggish for the remainder of 2024 and likely even so for 2025 unless there are signs the inventory digestion is more or less complete.

Valuation

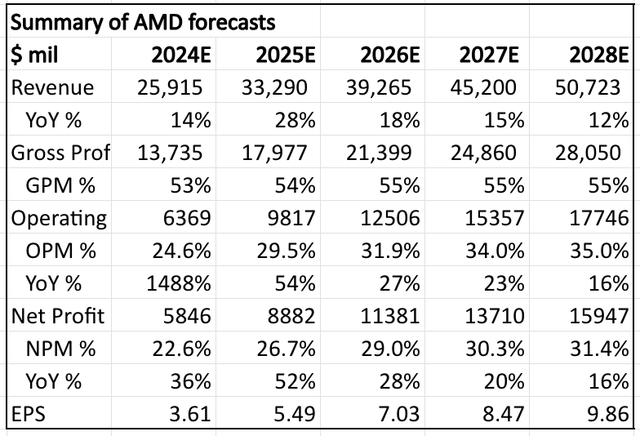

I am reiterating my financial forecasts for AMD, given that I have been pricing in that in 2024, both data center and client segment revenues grow due to continued market share gains and a strong product portfolio while embedded and gaming segment revenues fall due to continued weakness.

While the data center GPU segment is largely margin dilutive today, I expect this to continue to improve through 2025, and with growing data center and client segment revenues, this will help drive operating leverage in the business and thus, EPS CAGR of 29% from 2025 to 2028 compared to the 18% revenue CAGR over the same period.

My intrinsic value for AMD is $219, based on the same 35x terminal multiple and 12% cost of equity assumed. The slight increase in intrinsic value is mainly because the intrinsic value is now as of December 31, 2024, instead of the earlier January 1, 2024, as we are less than two months away from 2025.

My 1-year and 3-year price targets for AMD of $247 and $339 are reiterated. They imply 45x 2025 P/E multiple and 40x 2027 P/E multiple respectively.

Conclusion

There are several moving pieces for AMD despite its data center segment making up 45% of total revenues and 144% of operating income this quarter.

Even within the data center segment, it can be separated into the data center GPU and CPU segments.

Today, the data center GPU segment is undoubtedly the most important segment for AMD and demand is strong, but it continues to be margin dilutive to the overall business so if this improves, we should see AMD’s multiple improve.

In the data center CPU segment, while investors are increasingly less focused on this segment, AMD is doing well as it gained market share this quarter due to an acceleration in the enterprise segment.

The Client segment is seeing some green shoots, while the Embedded and Gaming segments remain relatively more challenged.

In 2025, I am looking for improvements in its margin profile, potentially a stronger Embedded or Gaming segment recovery, and continued strength in the Client and data center segments.

Great insights and analysis. I spoke about AMD in my last newsletter as well. I totally agree with you. The data Center CPU market is where they currently shine with their EPYC lineup, which leads the pack. They should continue to focus on the data Center GPU business and continue to heavily innovate.

Appreciate the analysis! When NVDA started blowing everyone away with their GPU revenue growth, I thought AMD would be the natural “fast follower” in the market. I came to believe, however, that I was trapped in the “Intel/AMD” historical framework, and that this time things would be different. Here the rub: a huge portion of GPU demand comes from the hyperscalers and META. They each are pursuing their own chips for internal use and several are achieving some success already. I expect that to accelerate from here at least as fast as interest grows in AMD GPUs. Consequently the competition for AMD GPUs will be NVDA plus its largest potential direct customers — and that’s going to be tough sledding.