CrowdStrike: Multiple Idiosyncratic Growth Pillars Amidst Noise

Strong momentum despite AI is killing software narrative

Software and cybersecurity has faced tough narrative challenges as investors were quick to sell all names in the bucket under the narrative that AI will kill software.

From a high level, the 4Q print, outlook for FY2027, strong and positive commentary on AI tailwinds and sufficient addressing of perceived AI headwinds should prove to investors that CrowdStrike should be an AI winner and not an AI loser.

Today, I will be covering these topics in the investment memo below:

CrowdStrike’s FY4Q26 print

Outlook for FY2027

Strength of the pipeline momentum

Falcon Flex traction

AI security products

Emerging businesses

Valuation

Conclusion

FY4Q26 print

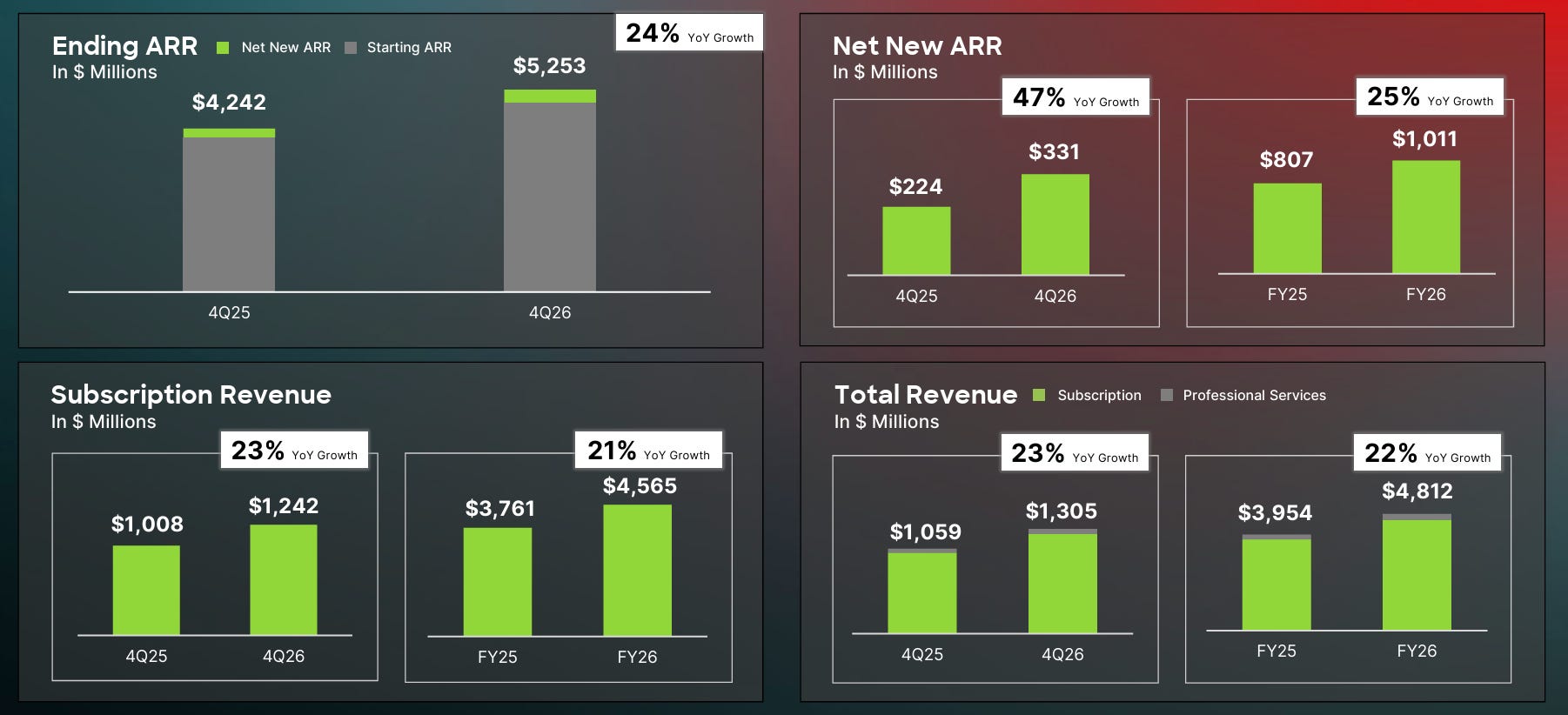

CrowdStrike’s ARR increased 24% year-over-year to $5.25 billion, 0.6% ahead of investor expectations, while net new ARR growth was 47% from the prior year.

Subscription revenue increased 23% from the prior year to $1.24 billion, 0.6% ahead of investor expectations.

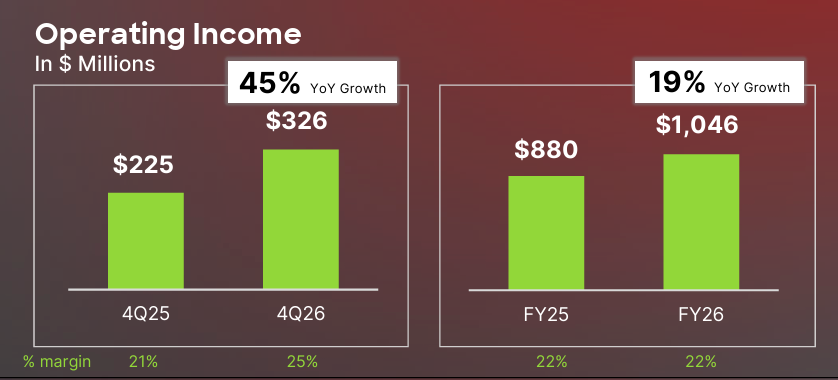

Operating income for the quarter was a record of $326 million, with operating margin coming in at 25%.

The FY4Q26 operating margin of 25% was ahead of both guidance and investor expectations of 24.5%.

This strong performance in operating margin was due to the outperformance in revenue, improvement in gross margin and continued sales execution.

CrowdStrike delivered earnings per share of $1.12, 1.8% ahead of guidance and investor expectations of $1.10.

The company generated $376 million free cash flows, translating to 28.8% free cash flow margin, ahead of guidance and investor expectations of 27%.

CrowdStrike’s FY4Q26 quarter demonstrated its ability to execute in terms of delivering profitable growth

Outlook for FY2027

The guidance for FY2027 was based on management’s confidence in the durability of CrowdStrike’s growth trajectory, profitability and expansion.

I think it is important to note that management stated that its pipeline in FY1Q27 is at a record high, growing 49% from the prior year, which in my view, also gives management further confidence and conviction in delivering the profitable growth it is looking to deliver in FY2027.

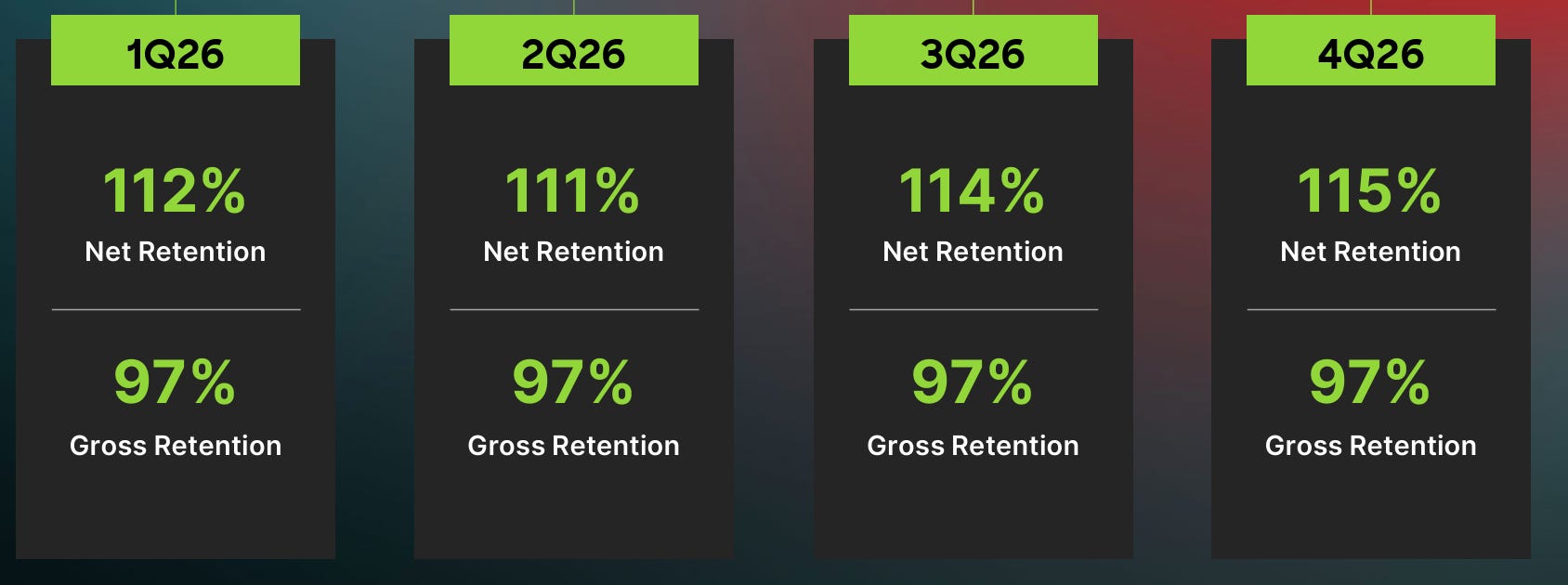

CrowdStrike’s net retention rate expanded to 115% this quarter, up from 114% last quarter and 112% at the start of the fiscal year, with the trend likely to continue as Flex utilization and expansion helps to drive a strong momentum.

Furthermore, it reflects growing momentum in fundamental tailwinds in its businesses, customer consolidation with platforms, AI proliferation and Flex adoption.

The company is also assuming minimal organic contribution from the acquisitions of SGNL and Seraphic (both of which were closed in February) in the remaining quarters of FY2027.

Lastly, management expects net new ARR seasonality to remain the same compared to FY2026, with 41% in the first half and 59% in the second half.

For the full year of FY2027, ARR is expected to increase 23.6% to $6.49 billion, suggesting the momentum in FY4Q26 will continue through FY2027.

This 23.6% ARR growth for FY2027 is ahead of investor expectations of 22.7%.

Revenue for FY2027 is guided to be $5.898 billion at the midpoint, or 22.6% growth from the prior year, ahead of investor expectations of 22% growth for FY2027.

Operating margin is expected to come in at 24.5%, ahead of investor expectations of 24.2% for FY2027.

Free cash flow margin is expected to come in at 30% for FY2027.

EPS is guided to $4.84 at the midpoint, 0.8% ahead of expectations.

In my view, the ARR growth guidance was ahead of expectations as it translates to ARR growth in FY4Q26 continuing for FY2027, suggesting strong ARR growth.

Strong pipeline momentum

In my view, it is important to emphasize how important the pipeline is for CrowdStrike investors.

Given that entering FY2027 the pipeline increased 49% from the prior year, this gives me further conviction that CrowdStrike has sufficient levers to pull and good visibility into the growth for the year ahead.

The 49% increase in pipeline does suggest the business momentum is strong.

What are the reasons for the strength in the pipeline?

Part of that is due to its customer commitment packages or CCPs that were from the outage from more than a year ago.