Is the software sector dead?

The software sector has seen a massive sell-off as it turned out of favor starting late 2025.

The IGV is down more than 30% from the October highs.

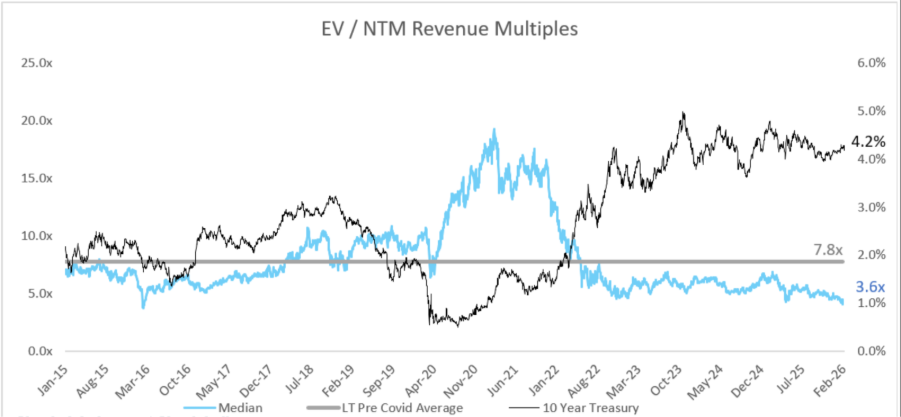

The median EV/NTM revenue multiples of software companies are now at a 10-year low of 3.6x.

As Benjamin Graham likes to say, in the short-term, the market is a voting machine.

The voting machine is now putting software companies in the “sell first and ask questions later” box.

As a result, we see software stocks being driven by sentiment and narratives and can be somewhat disconnected from reality and fundamentals.

One week, it can be Anthropic’s new product announcement.

Anthropic launched Claude Code Security and all the biggest cybersecurity firms like Palo Alto Networks, CrowdStrike and Zscaler are dead.

Another week, it can be about vibe coding.

“All the biggest cybersecurity firms will be vibe coded away”.

What is my view of all this?

I will share more about my channel checks I have done with IT executives running all types of companies and find out whether software is really dead.

But I think like any rational investor, I think this sell-off has gone too far.

There is no way vibe coding replaces the roles of CrowdStrike and Palo Alto Networks in the world.

I think the most crucial thing for software investors and cybersecurity investors to think about is what should the multiple for these companies be when the dust settles?

Today, we see significant multiple compression from the 5x median EV/NTM revenue multiple in 2024 to 3.6x today, which is a 30% multiple compression.

Multiples are a function of growth and risk.

Risk has certainly gone up for software stocks due to the higher uncertainty about their future.

While I do think most of the top tier software and cybersecurity names will adapt and thrive in a new “AI world”, what happens 10 years from today I genuinely do not know because of how fast AI is changing and improving.

As such, the higher uncertainty warrants a lower multiple.

Growth is another consideration and here, there will be a dispersion in my view.

There will be 2 buckets of software and cybersecurity companies: The ones that innovate and the ones that do not.

AI will bring about new opportunities and software companies need to pivot fast enough to benefit from the hyper-growth potential of these new growth areas.

The software companies that innovate fast enough will almost certainly see faster growth rates than the companies that do not, and with that, the multiples will disperse over time.

In my view, we are already seeing the dispersion, although the market does not recognize the winners from the losers and is selling everything software on narratives.

The “AI will kill all software” narrative is getting too out of hand in my view, and the correct way to phrase it is “AI will kill software companies that do not innovate fast enough”.

Realistically, even for the dinosaur software companies out there, the truth is that the cloud migration theme will continue alongside this AI theme and there will continue to be multiple growth tailwinds for software companies.

I met a CEO of a large industrials business company, and they continue to migrate to SAP.

I met a CTO of a large consumer business company and they continue to expand with the likes of Snowflake and Workday, amongst others.

The reality is that companies do not have the desire to build their own Workday, Snowflake or SAP, at least not in the near to medium term.

“The market is a pendulum that forever swings between unsustainable optimism (which makes stocks too expensive) and unjustified pessimism (which makes them too cheap)”.