Microsoft: A turning point

Accelerating growth and resilient business fundamentals

This could be the start of the turning point for Microsoft MSFT 0.00%↑ .

Not only did Azure beat significantly this quarter, but the beat was also driven by non-AI workloads, which was strong across the board, while more capacity was able to be brought online this quarter than expected for the AI side of Azure.

This strong result is expected to translate into stronger-than-expected Azure growth next quarter, driven by the stronger AI demand and better execution from non-AI workloads.

Microsoft also addressed noise surrounding the data center lease cancellations in the press, reiterated capital expenditure spending going into 2026, and suggested that demand continued to outstrip supply and that this dynamic will continue for some time more.

While the scaling of AI infrastructure is expected to impact margins, Microsoft has also executed well to preserve margins by improving on cost efficiencies.

Today in this article, I will be going through:

Exceptional results

PBP and MPC segments

Guidance exceeds

Azure growth back on track

Addressing data center lease cancellations

Valuation

Conclusion

Exceptional results

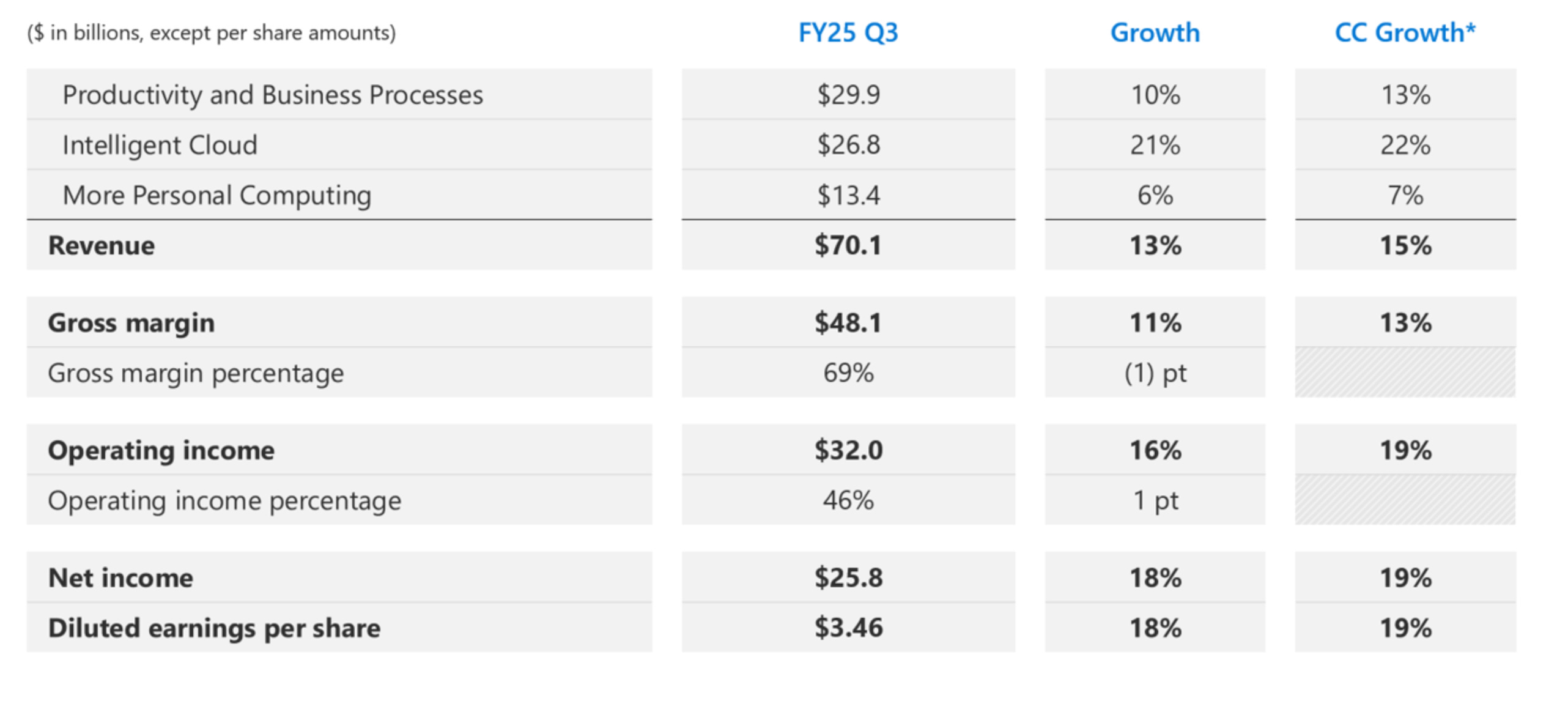

Microsoft had an exceptional FY3Q25 quarter.

Total revenue grew 15% from the prior year on a constant currency basis, driven by broad based strength across Productivity and Business Processes (“PBP”), Intelligent Cloud (“IC”) and More Personal Computing (“MPC”) business segments.

Commercial bookings in FY3Q25 also grew 18% from the prior year on a constant currency basis, fuelled by an additional OpenAI commitment.

Microsoft also beat expectations on profitability as gross margins of 69% and operating margins of 46% came in 53 basis points and 145 basis points ahead of consensus expectations respectively.

Operating expenses also came in more than 1 percentage point below consensus expectations.

Despite seeing company gross margin fall 1 percentage point from the prior year to 69%, this was due to the scaling of AI infrastructure, which was expected.

However, in my opinion, the beat in gross and operating margins demonstrate Microsoft’s ability to execute and focus on improving cost efficiencies.

During the FY3Q25 quarter, Microsoft continued to reduce inefficiencies by reducing the number of managers and developing higher performance teams, while slowing the pace of headcount growth.

Diluted EPS came in at $3.46, growing 19% from the prior year and beat consensus expectations by 7.5%.

On the balance sheet side, cash paid for PP&E of $16.7 billion was lower than consensus of $17 billion, and this was the first time capital expenditures missed since last year though this was still an increase of 6% sequentially.

The total capital expenditures for FY3Q25 was $21.4 billion, down 5% sequentially and 6% below consensus.

PBP and MPC segments

I will briefly comment on PBP and MPC here and go deeper into IC in the next section.

Within the PBP business segment, revenues beat by 1 percentage point. Microsoft 365 Commercial Cloud grew 15% from the prior year on a constant currency basis and was ahead of expectations, with commercial seat growth growing 7% from the last year due to strength in SMB and frontline worker offerings.

During the call, management shared that Microsoft 465 Copilot now has hundreds-of-thousands of customers and is up 3x over the last year, with a record number of customers returning to buy more seats.

Dynamics 365 grew 18% from the prior year on a constant currency basis while LinkedIn growth continues to stabilize though it downticked 1 percentage point from last quarter to 8% growth from the prior year.

Within the MPC business segment, revenues beat by 5.6%.

The MPC upside came from broad based strength, with a considerable beat in Search & News Advertising ex-TAC which grew 23% from the prior year on a constant currency basis compared to the mid-teens guidance.

Windows OEM & Devices revenue beat expectations driven by tariff uncertainty that kept inventory levels elevated, which management expect could reverse in 4Q.

This is highlighted by the 3% year-on-year constant currency growth this quarter compared to the guidance for next quarter to decline low-to-mid single digits.

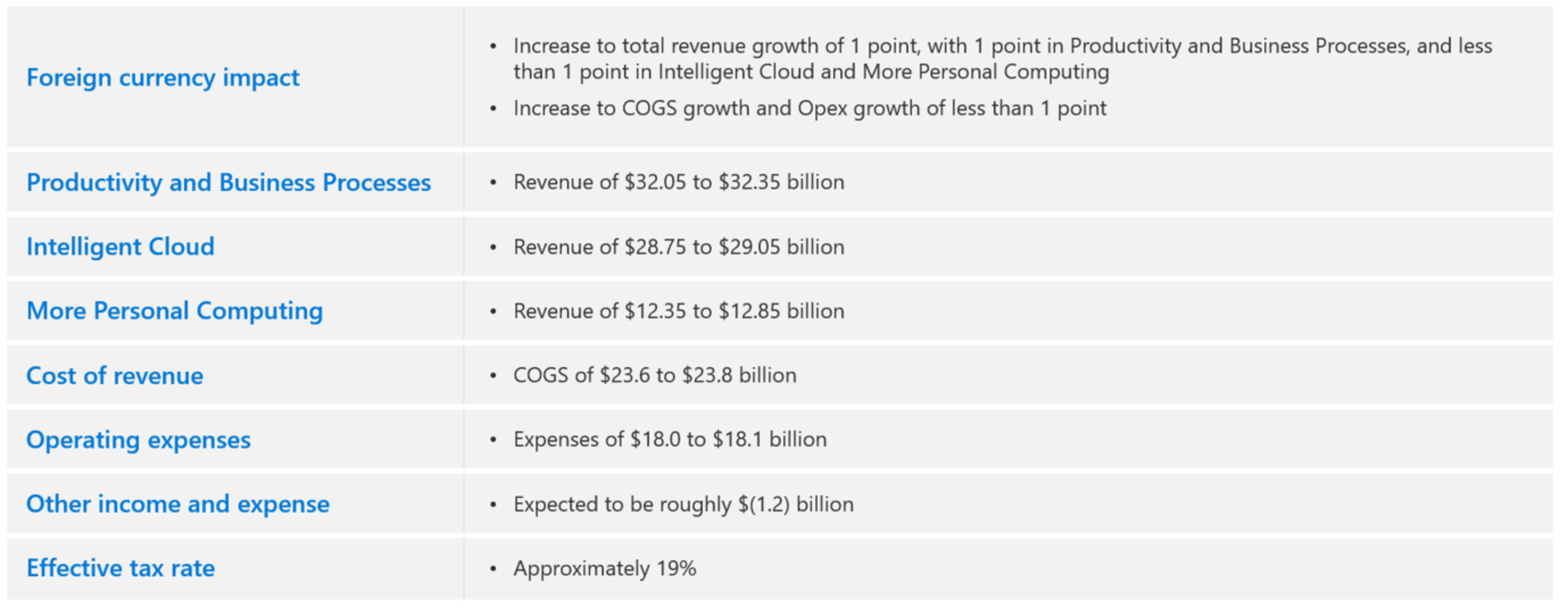

Guidance exceeds

FY4Q25’s revenue guidance at the high end in the constant currency basis came 1 percentage point higher than consensus expectations.

Azure’s growth is expected to be between 34% to 35% on a constant currency basis in FY4Q25, higher than the 32% growth expected by consensus expectations.

The stronger-than-expected Azure growth is due to the stronger AI demand and better execution from non-AI workloads.

Operating profit margin guidance for FY4Q25 came in at 43.4% driven by some timing shift from 3Q into 4Q.

FY2026 capital expenditures guidance was also reiterated from January quarter, guided to grow at a lower rate than FY2025 and include a greater mix of short-lived assets.

Azure growth is back on track

Finally, within the IC business segment, revenues beat consensus expectations by 270 basis points.