Today, we look at what’s next for Nvidia NVDA 0.00%↑.

I had the opportunity for a call with Nvidia CFO Colette Kress to understand the future opportunities for the company from the inside lens.

Here’s what I will cover in this deep dive into Nvidia:

Sustainability of revenue growth

Nvidia’s margin profile going forward

Demand visibility through 2027

Sources of demand

Product roadmap

Groq 3 LPX opportunities

Capital allocation

Supply chain

Valuation

Conclusion

Revenue growth sustainability

We have seen investors talk about this since 2024, and every single time, Nvidia continues to defy the odds.

Compute has remained a limiting factor with demand far exceeding supply, but in 2026, investors are starting to think that we could see some digestion or slowdown in the next 1 to 2 years.

Some buyside portfolio managers I spoke to recently expect some form of inventory digestion from the hyperscalers in the next 1 to 2 years as they have been relentless in their investing in AI infrastructure since the launch of ChatGPT.

We look into not just what Nvidia is saying, but what the customers and supply chain is saying about the next year or two.

Inevitably, the discussion comes down to hyperscaler spending given a large portion of their huge capital expenditures are going to their buildouts of compute capacity.

Speaking to hyperscalers, it suggests to me that they are already starting to plan their 2027 compute capacity buildouts.

This ties in with what Nvidia is suggesting as well, that they are seeing visible demand signals for 2027 that suggest it is looking to be another strong year for the company.

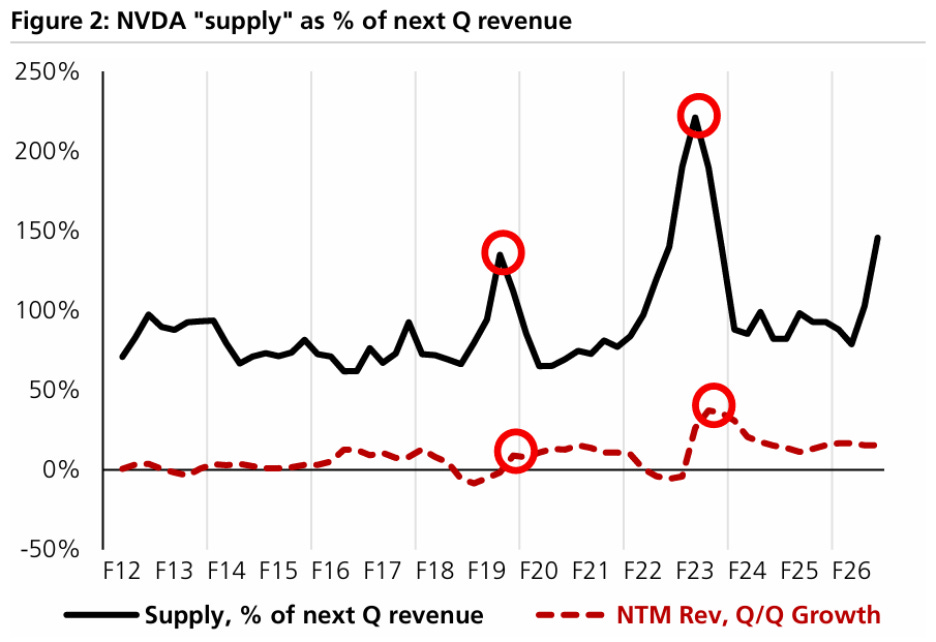

Furthermore, in my view, Nvidia’s supply, which includes inventory purchase commitments, balance sheet inventory and long-term supply obligations, has not been noticed or given weight by the market despite seeing very strong growth.

Last quarter, Nvidia’s inventory purchase commitments and balance sheet inventory increased significantly, up $25 billion or 56% sequentially.

This quarter, this figure accelerated again, up $46 billion or 66% sequentially.

I think it is important to note that Nvidia has been procuring items like memory over a longer timeline, so this number is now skewed more by longer term items compared to in the past.

Even after adjusting for these changes, the current supply figure implies that Nvidia has sufficient supply for quarterly revenue in the $100 billion range within a couple of quarters.

If I were to tie this in to what management said in its most recent call, management noted that the increase in balance sheet inventory and inventory purchase commitments is to support the buildout beyond the next several quarters.

Furthermore, when we dig into the notes in the 10-K, it suggests that substantially all of this amount is in support of F2027 revenue.

Nvidia has already secured all the components including memory through calendar year 2026 and now is focusing on 2027.