The year of the stock picker: 25 stock ideas for 2025

2025 market outlook, themes to look out for in 2025 and 25 stock ideas

2024 was a good year for the stock market, with the S&P 500 up 23% for the year

This is the second straight good year for the stock market as the S&P 500 also gained 24% in 2023.

This has prompted some calls that the market is in a bubble, but I believe that while the overall market valuation may seem stretched, there are pockets of opportunity for superior investors in 2025.

I believe 2025 is the year of the stock picker.

Today in this article, I will be going through:

2025 market outlook (Valuation, economy, sentiment, rates)

Themes for 2025

25 stock ideas for 2025

If you don’t already know, I just launched Outperforming the Market on 2 January 2025.

Subscribers that subscribe to Outperforming the Market in the first week of launch (by 9 January 2025) get a special 20% off discount that can be found below ($255 per year).

This special rate is locked in forever, even if I increase prices in the future.

Year of the stock picker

When we look at the overall market level, valuations appear to be on the expensive end.

Equity risk premiums are currently low.

For those who are new to the term, the equity risk premium is basically the excess return earned by an investor when they invest in the stock market over a risk-free rate.

Equity risk premium is the reward or return that compensates investors for taking on the higher risk of equity investing.

When equity risk premiums are low, investors are not reward sufficiently for taking on the higher risk of investing in equities.

As of November 22, 2024, the equity risk premium is at the 67 percentile and 94 percentile from 2000 and 2010 respectively.

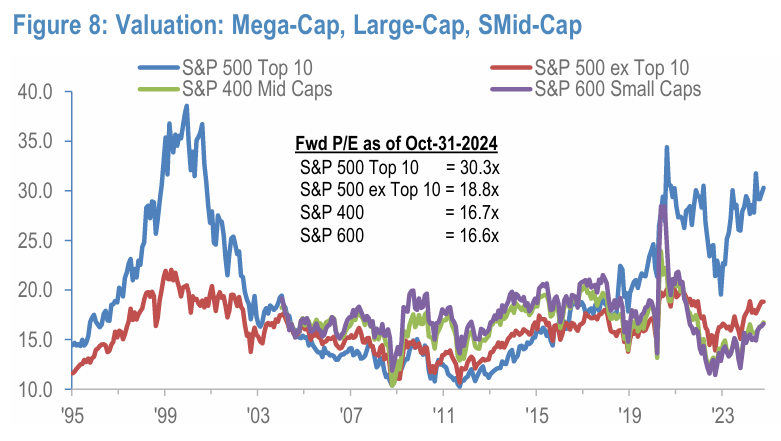

Valuation multiples are stretched

The S&P 500 is trading at a forward multiple that is close to the high end of its range.

As such, the probability of further multiple expansion on the index level is unlikely in 2025, and most of the S&P 500’s gains in 2025 should come from earnings growth (more on that later).

However, the expensive valuation at the market or index level is largely attributable to the top 10 stocks in the S&P 500.

As you can see below, the top 10 stocks in the S&P 500 are at 30.3x forward P/E multiple, above its average since 1995, largely due to growing profitability, unlike what we saw in the dot com bubble in 2000.

However, the S&P 500 excluding the top 10 stocks, S&P 400 mid caps and S&P 600 small caps are all still trading at somewhat reasonable valuations at 18.8x, 16.7x and 16.6x forward P/E multiples respectively.

The overall market level may seem expensive, but most of that is due to the 10 largest stocks, while below that, we see more reasonable valuations.

That’s why 2025 will likely be a stock picker’s year.

Economy, corporate sentiment

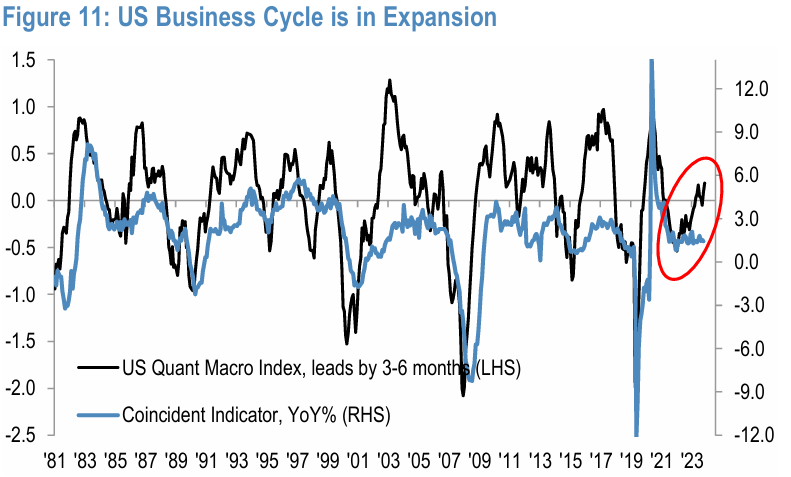

Business cycle still in expansion mode

The US remains the global growth engine with the business cycle in expansion, healthy labor market, broadening of AI-related capital spending, and prospect of robust capital market and deal activity.

As shown below, the US business cycle continues to be in the expansion mode.

An easing monetary cycle in combination with still healthy corporate and household balance sheets should prevent the business cycle from rolling over in the next few quarters.

Corporate sentiment

Corporate sentiment on earnings is actually rather strong.

In fact, we are at the 96% percentile in terms of sentiment on corporate earnings for the S&P 500, which highlights that corporates are seeing a more positive outlook for 2025.

Likewise, corporates have a positive outlook on margins,

Corporate sentiment on margins for the S&P 500 is currently at the 98 percentile since 2010.

Once again, this highlights that the sentiment corporates have on margins on the S&P 500 level is positive.

Rates

After an eventful December FOMC meeting, there was a re-pricing of the number of rate cuts in 2025.

Currently, only 1 rate cut is priced in for 2025.

However, I do think that with such conservatism in the market on rates, there is actually upside for equities in the form of more than expected rate cuts in 2025.

But I think the most important thing to note is the green line (shown below), that no matter how fast rates are being cut, they are expected to come down in 2025, 2026, 2027 and beyond.

Rates continue to be on a downward trajectory.